I’ve bent many an ear over the years about the idea of permanent online storage. Since Google just introduced a new online storage service with simple, linear fees, this seems like a good time to actually run some numbers.

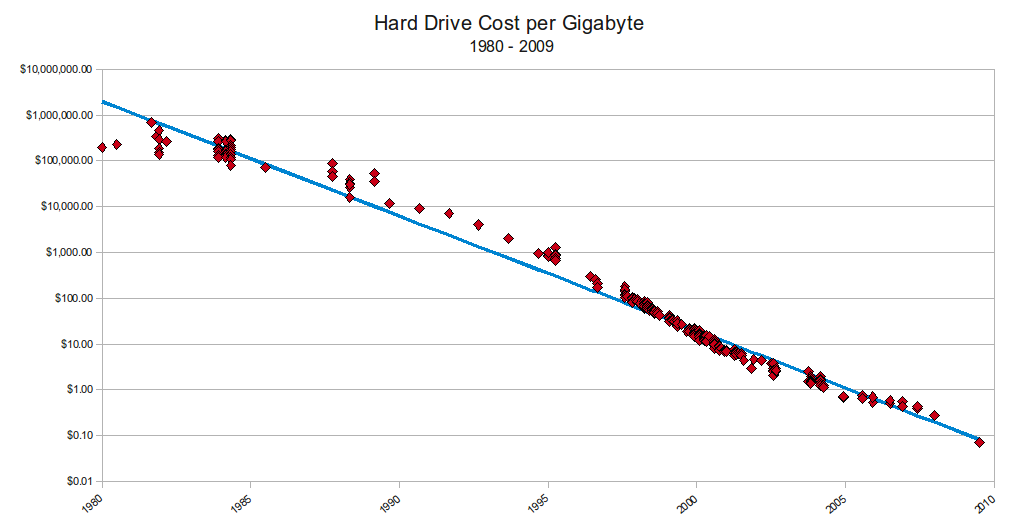

First of all, stating the obvious: The cost of local storage (in other words, hard drives) has been dropping exponentially for a couple of decades. And, when I say ‘exponentially’ it’s not a figure of speech. Here’s a well-researched graph of storage costs plotted with a logarithmic Y axis by Matt Komorowski:

Matt provides a nice if overly-precise formula for the shape of the curve: cost per gigabyte = 10^(-.2502*(year-1980)+6.304. Fair enough.

I’m now going to take a big leap, and presume that online storage costs are at least vaguely proportional to hardware storage costs. Something like k1 + k2*10^whatever, where k1 is the flat cost of providing the service, and k2 is the factor by which online, networked storage (for a year) is more expensive than local storage (for as long as your harddrive lasts). I’m also going to assume that as data size grows, the relative importance of k1 diminishes, so I’m going to ignore it. Pretty much all the coming math still holds for non-zero but non-gigantic values of k1, anyway.

In any case, Google thinks that k1 is zero too. Look at their pricing schedule:

25G $2.45/month

100G $4.99/month

200G $9.99/month

400G $19.99/month

Once you buy 100G or more, the price is a nickel per gig per month, period. That’s $.60/year. Matt’s curve says that a gig of harddrive space should cost $.02 in 2012, so that gets us k2 = 30.

Another thing that’s exponential is compound interest. Even in these stagnant times it’s still possible to buy a long-term annuity or 30-year bond that produces a non-zero return.

So, picture this: Instead of paying Google $5/month for my storage, I give them three year’s worth of fees all at once: $180. Google invests that money at a rock-solid 1% interest per annum. (I can only assume that Google has better investment opportunities than that, but I’m being as conservative as possible.)

The first year, Google will spend 60 of those dollars, leaving $120. The $120 earns $1.20 in interest, leaving Google with $121.20. In the second year, the storage is quite a bit cheaper, so at the end of year two Google has about $93 left.

A few years down the line, things get interesting:

Looks to me like I didn’t buy three years of storage for $180 — it looks to me like I bought 1,000,000 years of storage. And, I overpaid.

Inflation, explained

My numbers are not adjusted for inflation. That’s OK, though, because the Matt Komorowski curve (officially known as Kryder’s Law) isn’t adjusted for inflation either.

Other things inflate, though. So we need to invest our principal at a rate greater than inflation or k1 will eventually become significant and devour our original investment.

Physics, dismissed

It’s always risky to extrapolate from past data, especially where exponential graphs are concerned. I won’t be shocked if storage /stops/ getting cheaper in my lifetime. Fortunately, though, the inflection point in the cost graph is in 2022. At 1% interest, we only need the current trend in storage cost to continue for a decade. If we’re able to invest at 3%, the graph inflects in 2019.

So, we don’t need current technology trends to continue forever — just for a few more years.